November hiring highlights strengths of current economy. The transportation, warehousing, construction and manufacturing sectors created a combined 112,000 jobs in November. Growth in these fields reflects, among other factors, the ongoing demand for more residential and industrial space to support an expanding population that is relying more heavily on delivery. Added manufacturing positions correlates with greater U.S. factory output to suggest that supply chain disruptions are no longer worsening. Many retailers are nevertheless enlarging inventories to avoid future shortages, increasing the demand for warehouse space.

Fewer service jobs indicative of near-term hurdles. Besides subdued hiring by hotels, bars, restaurants and entertainment venues last month, other retailers cut staff in November. The 20,000 fewer retail trade positions may reflect a greater reliance on delivery from online or omni-channel stores as well as supply-induced constraints from shipping delays. Going forward, infection concerns may become a greater factor. While the full implications of the omi- cron variant are still unknown, a winter increase in COVID-19 cases is possible. Holiday travel may still drive demand for hotel rooms, however. Occupancy during Thanksgiving surpassed the 2019 level.

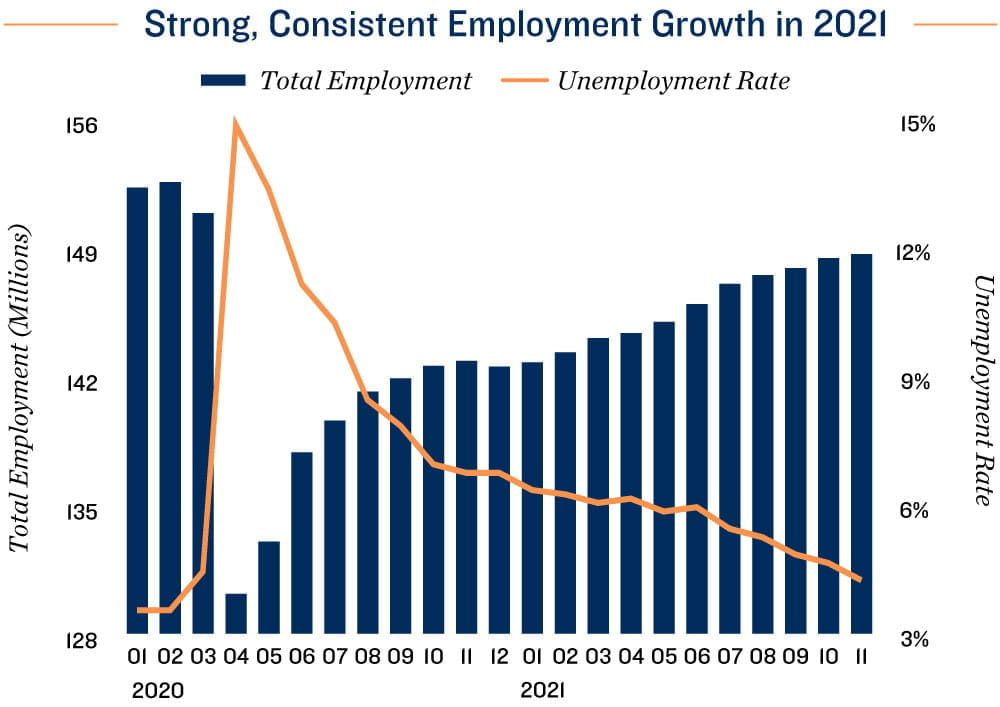

Year in Review

Sizable, consistent gains distinguish 2021 after volatile 2020. Following last year’s roller coaster, 2021 will go down in the record books as the strongest single calendar year for job creation in modern history. Payrolls expanded by over 6 million jobs this year, building on the 13 million positions recovered in 2020 to return the employment base to within 2.6 percent of the pre-pandemic level. This represents a faster recovery than during the global financial crisis, when it took 26 months for the workforce to climb to within the same margin of the pre-crisis high.

Labor-shortage-induced inflation prompts Fed concern. More job openings relative to job hunters helped drive average hourly earnings up 4.8 percent year over year. Ignoring volatility in the pandemic, this is the fastest rate of wage growth in over 10 years, further contributing to already steep inflation. Concerns over a spiraling feedback loop may accelerate the Fed’s timetable for tapering bond purchases and hiking interest rates. This would raise the cost of borrowing for real estate investors, potentially affecting leveraged returns.

18.5 |

4.8% |

|

Million Jobs Added SInce April 2020 |

YOY Increase in Average Hourly Earnings |

Sources: Marcus & Millichap Research Services; Bureau of Labor Statistics